The revolution and development of new fintech payment tools are crucial for eCommerce because of their ever-growing popularity, but they do not eliminate the need for traditional payment methods. Many businesses still use credit and debit cards, bank transfers, cheques, cash, and physical point-of-sale (POS) terminals to manage customer payments.

It is not so much a matter of choosing between traditional and digital payments, but of finding the ideal balance so that both methods can coexist in harmony and fit the needs of each company’s potential audience.

At PayXpert, we are aware of the importance of traditional payments and fintech payment tools for business. That is why we support both methods. Our goal in this post is to make a comparative analysis of the payment processing offerings of traditional banking and fintech.

Join us and do not miss it.

What are fintechs and traditional payment methods?

Technology and the new digital era have brought about a major transformation in all sectors of the global economy, including the financial sector. This phenomenon has given rise to fintech, a concept that summarises the blending of technology and finance (financial technology) and covers a wide range of areas or verticals: payment methods, alternative financing, personal finance, wealth management, neobanks, cryptocurrencies, insurtech, etc.

The fintech phenomenon has not only had a major impact on consumers’ experience with brands, but has completely changed and restructured the financial services sector.

On the other end of these developments, we find traditional payment methods, which we have defined as those payment methods commonly used by commerce, especially physical commerce, and that have been passed down through the generations. Cash or cheque payments, credit and debit cards or cash on delivery are some examples of traditional payments.

Technological developments and the COVID-19 pandemic have become two important drivers of change in eCommerce. In fact, they have favoured relevant new forms of payment in the market, which we will discuss in this post.

Overall situation of payment methods

It is not surprising that payment methods are at the centre of the fintech phenomenon given the appeal of this particular segment of the financial system. We have compiled relevant information about this trend from the Journal of Business Studies:

- Payment services revenues have increased at an average annual rate of 6.8% globally since 2010, reaching $1.27 trillion in 2017.

- Projections for the next ten years remain favourable, with payments expected to generate more than $1 trillion in new revenue over the next decade, reaching $2.42 trillion by 2027

- The highest growth will be in emerging economies, which will drive 70% of growth.

- The accelerated growth in these countries (mature economies such as Western Europe, North America and some Asian countries, and fast-growing economies, such as Mexico, Russia or China) is related to the slower development of the financial sector, which brings with it a higher penetration rate for digital payment methods.

While digital payment processing has gained in importance today, traditional payments are still necessary for the financial management of many businesses: retail, eCommerce, hotel chains, etc.

PayXpert connects merchants directly to the world’s key payment methods, enabling them to accept payments and optimise growth across the online and offline channels that customers engage with.

Of course, technological innovation in the payments industry has not only triggered change, but has also attracted new competitors, forcing merchants to innovate and improve their offerings. These developments have taken place not only in infrastructure but also in support, service, and security.

Most popular traditional and fintech payments

The new digital age is revolutionising the financial sector. How is it doing so? Through the development of new payment platforms for example. Digitalisation remains to be the main challenge for national banks and physical merchants, a change that starts by placing the customer at the centre of their strategy. Traditional banks face a much more demanding environment marked by competition and the emergence of new players (fintech).

Although the fintech ecosystem is made up of a wide range of verticals, we wanted to draw attention to pay in this post.

Most popular digital payment types that fintech has brought about:

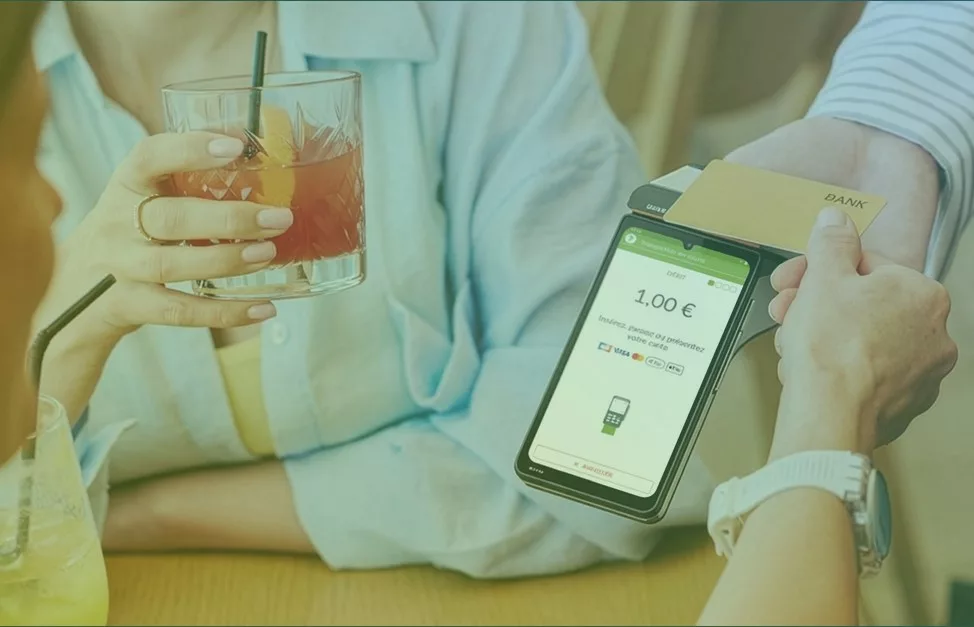

This is a form of payment that does not involve the use of cash or a credit card. This payment acceptance method is possible thanks to the technological advances in the financial industry, based on voice recognition, payment with QR code or facial biometrics (face to pay). These options were initially developed in Asia, with Tencent and AliPay.

- Digital wallet (eWallet)

These are a digital version of traditional wallets that allow financial transactions to be carried out through electronic devices (smartphone, tablet, computer), as well as storing useful data for payments, such as credit card information. This payment way to pay has been very popular in countries such as Argentina and the United Kingdom.

- P2P (peer to peer) transfer

Peer-to-peer money transfers are money transfers between individuals carried online and through electronic devices. These operations are made possible by linking a card or bank account with an application. It is a fast and straightforward process and an excellent opportunity to attract new customers.

This is a newly digitised version of card payments that not only enables PSD2 compliance but also provides security, trust, and simplicity. It protects the PAN number with an encryption system that issues a unique code (token) that replaces the real number during the transaction.

- Wearables

These are small technologies that accompany the user at all times, such as a wristwatch turned into a smartwatch or an activity bracelet that enables contactless payments. They work in much the same way as a contactless card, only requiring the POS to be close to the device.

- Mobile payment

These are the transactions made through mobile devices. Over the years, many mobile applications specialising in payments have been developed, which speeds up processing times and improves security. This form of payment has been very successful in European countries such as Spain and Latin American countries such as Colombia.

Fintechs are said to offer a much wider variety than just the traditional payment methods offered by traditional banking, as well as a different target audience and faster scoring. However, traditional payments are still necessary for much of today’s business. We have compiled them below:

It is a certified document with the amount payable to the bearer, which is exchanged for cash. It is an ideal form of payment for businesses with a medium to a high volume of incoming cheque payments, from non-profit charities to mail-order companies.

- Cash

This is the most familiar and traditional type of payment, as it involves the exchange of physical banknotes or coins to purchase or contract for goods and services. In the last year, there has been a reduction in the use of cash globally, driven by the Covid-19 pandemic.

- Cash on delivery

It is commonly used for distance purchases and consists of paying the cost of the order placed online to the person who physically delivers it to the customer’s home.

- Credit and debit cards

This is the most widespread type of payment in the world and refers to the use of cash that a user has in their bank account at the time of purchase. They allow you to pay in instalments or make a purchase without physically handing over the amount. When you pay with a debit card, the money is immediately withdrawn from your account.

It is worth noting that, for many businesses, choosing payment acceptance means is a complex process. Sometimes, it is not a matter of deciding between digital payments or physical payments, but of selecting the solution that best suits the needs and features of the target audience. Currently, traditional financial institutions have an active strategy of acquiring and investing in new financial technologies.

The key features of fintechs

Talking about the features of fintechs is like asking what features today’s financial technology solutions for business should have. In other words, those the new generations of millennials and centennials feel familiar with.

We have summarised them in the following points:

- Digital channel sophistication. It drives the creation of end-to-end experiences through omnichannel strategies.

- Data management. Data analysis is a driver of continuous improvement in the bottom line, and in the consumer experience.

- Virtual reality and augmented VR and AR-based devices maximise the user experience with new environments.

- Virtual assistants. Technological developments are also making it possible to create advanced systems that automatically understand and predict consumer behaviour.

- Business intelligence. Dashboards based on business intelligence allow you to monitor activity peaks, analyse customer behaviour across all channels, and make better decisions based on real data.

- Flexibility. Fintechs help money management, offer a variety of payment methods to carry out transactions, simplify the required documentation and allow new metrics to be taken to analyse consumer behaviour.

The impact of COVID-19 has changed customer preferences, especially when it comes to the use of loans, social commerce and digital transformation. Contactless payments are the way forward for consumers, but mobile payments also seem to be here to stay.

A couple of years ago, cash used to be king, but now it is slowly disappearing. Germany, for example, has significantly increased the use of debit and credit cards since the pandemic, but it has not been the only country. At some point, digitalisation will continue to evolve, so even the smallest kiosk will need to have a payment terminal.

If you need to increase revenues and reduce costs, it is essential to offer valuable payment experiences to your customers.

Are you looking for disruptive solutions that enable innovation in your business? At PayXpert, we can help you with our traditional and digital payment solutions.