Today’s businesses face a growing need to synchronise activity across multiple platforms. To appeal to consumers and meet them wherever they may be most comfortable, a company has to present a united front between its website, app, social media presence, and in-person location if applicable. Generally, this means keeping information, inventory, and presentation up to date across all of these areas. However, these days it also has to mean facilitating omnichannel payments.

For those unfamiliar with the term, the idea of omnichannel payments is simply that of a company accepting payments in various ways. For instance, if a company has a store, website, app, and social media profile, said the company would be facilitating omnichannel payments by enabling transactions directly through those different entities. This is as opposed to having a social media account to link a customer back to the website when the time comes to make a transaction.

Empowering omnichannel payments is entirely feasible for modern businesses. However, it does require the use of some relevant technologies.

Chat Systems

When we think of mobile payments, it tends to be in the context of apps. And to be sure, any modern business looking to bring about omnichannel payments should enable its app to handle direct transactions. However, we’re also beginning to see more in payments made through chat systems. Our post on WeChat Pay as “a mobile payment storm from China” delved into this idea. The Tencent mobile app Wechat has sparked a significant trend with its WeChat Pay feature. This tool within the app facilitates financial transactions and sets the stage for businesses to engage paying consumers through chats. With WeChat Pay — and conceivably even Venmo and the Cash App — companies can directly interact with customers and receive payments (for goods, services, subscriptions, etc.).

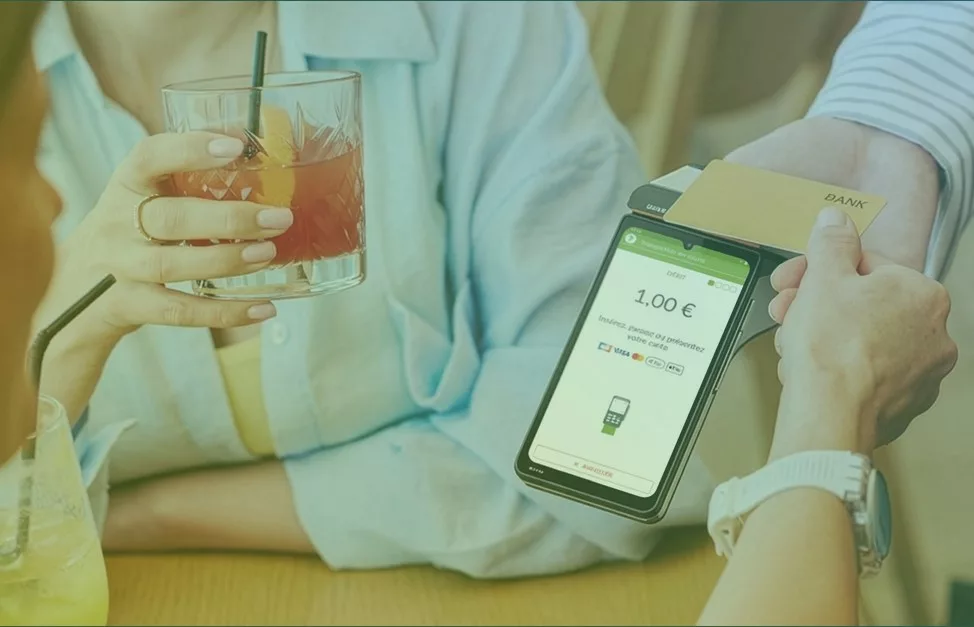

POS Devices

When working to bring about omnichannel payments, it’s also vital for any business with a brick-and-mortar presence to recognize that in-store transactions can also take many forms. While many consumers still pay with traditional credit and debit cards, or even cash, many others prefer more modern options such as contactless swipes and cryptocurrency transactions. This may seem complicated, but the reality is that it just means stores need to be stocked with more modern point-of-sale devices. The best of them can handle all the payment methods mentioned above with minimal hassle, giving customers the flexibility to pay however they, please.

Blockchain

Blockchain technology is widely associated with Bitcoin and other cryptocurrencies. But it doesn’t necessarily have to be tied to them to be useful. A guide to blockchain uses beyond Bitcoin by FXCM covers a variety of alternative applications, including potential use by businesses. The guide states that blockchain can facilitate “payments taking place between organizations and their clients,” potentially reducing fees and expediting transactions, although the infrastructure is still not there. This can be particularly useful for online and app-based transactions. A company today can use blockchain tech to make such transactions quicker, cheaper, and more reliable.

AR & VR

Augmented and virtual reality don’t represent existing “channels” where most businesses are concerned. However, many believe they will soon have a very active place in modern commerce alongside social media and mobile apps. And for that reason, it would be worthwhile for any business seeking to empower omnichannel payments to look into implementing AR and VR ahead of the curve. Nielsen’s look at AR and VR driving “omnichannel 2.0” explained how the technologies could be of use with a simple but significant example: Imagine that instead of going to a grocery store, you put on a headset and take a virtual tour through a store, viewing information about products and filling your cart. Then, imagine you can pay through the same AR or VR app. At PayXpert, we always have one eye on the future, and our minds are set on adding value in and around the payment experience.

Social Commerce

Finally — and maybe most importantly, in today’s business environment — companies seeking to bring about omnichannel payments must also embrace social commerce. Two years ago, Retail Dive cited a study on social payments that revealed that some 55% of consumers claim to have made a payment through a social media channel (like Facebook, Instagram, or Pinterest). Undoubtedly, that number would only be higher if the same study were conducted today. This means that a subtle but significant shift is now in order. Rather than using social media to direct customers to their websites or apps, companies need to invest in social commerce features that enable payment processing within social channels.

With these methods and technologies, a modern company can take significant steps toward empowering multichannel payments. This, in turn, will likely lead to higher customer satisfaction and more business.