Fintech and other strategies to increase sales.

The reality of the current economy and trade is characterized by the increasingly prominent electronic commerce, as well as new solutions and payment gateways adapted to this new form of the global economy. However, the concerns of companies remain the same: finding strategies to increase sales, either in physical commerce or e-commerce. At this point financial technology companies like PayXpert emerge and offer both businesses and users financial tools adapted to a globalized and online economy.

Technology in the form of payment gateways, data management and management control.

E-commerce has opened the doors to flexible and versatile commerce for its own sake, connecting companies and clients from all over the world. Nevertheless, the considerable power of payment automation involves a great weight of responsibility to maintain the transparency and honesty required by users. This new era will mean a revolution in how we understand our business (as companies) and our day to day (as consumers). Focusing on this new paradigm, we bring you three key aspects to keep in mind to adapt your company to this new era for trade.

Cloud management of payment cards.

E-wallets are the future of transactions and commerce and they undoubtedly represent one of the best strategies to increase sales, while saving time and money for our clients. They allow their users to store cards (whether credit, debit, revolving, prepaid, business cards…) in order to make e-commerce payments in a simple and safe way. This opens up a new market niche for financial institutions: getting its users to set their card as the “main card”. Studies show that consumers spend more on both physical and electronic commerce, when they designate a card as “main” or “default”. But even if the financial institutions manage to get their clients to automate their cards in one of the main e-wallets, the logos of cards (and consequently of the brand) become invisible, which makes them less relevant in other possible purchases users can perform. In order to remain relevant and convince their clients to set their cards as main, these entities should consider helping customers with such a costly task. An example of this is the agreement between Chase and PayPal, in which Chase Freedom card users receive 5% of the expense made through PayPal. In addition, banks would be responsible for updating PayPal accounts in case of card expiration, or changes in the user’s profile or password.

Invisible payments.

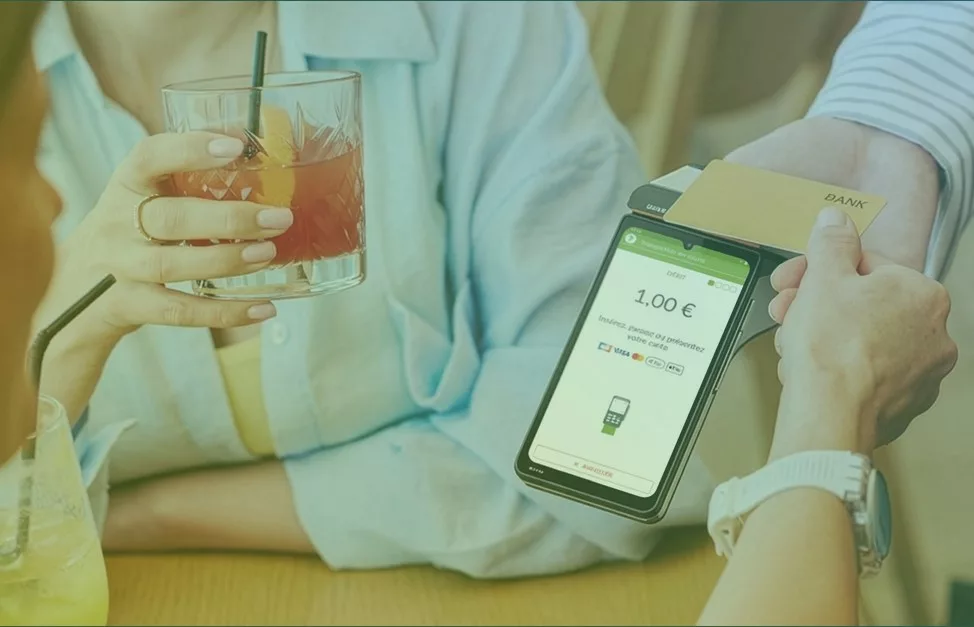

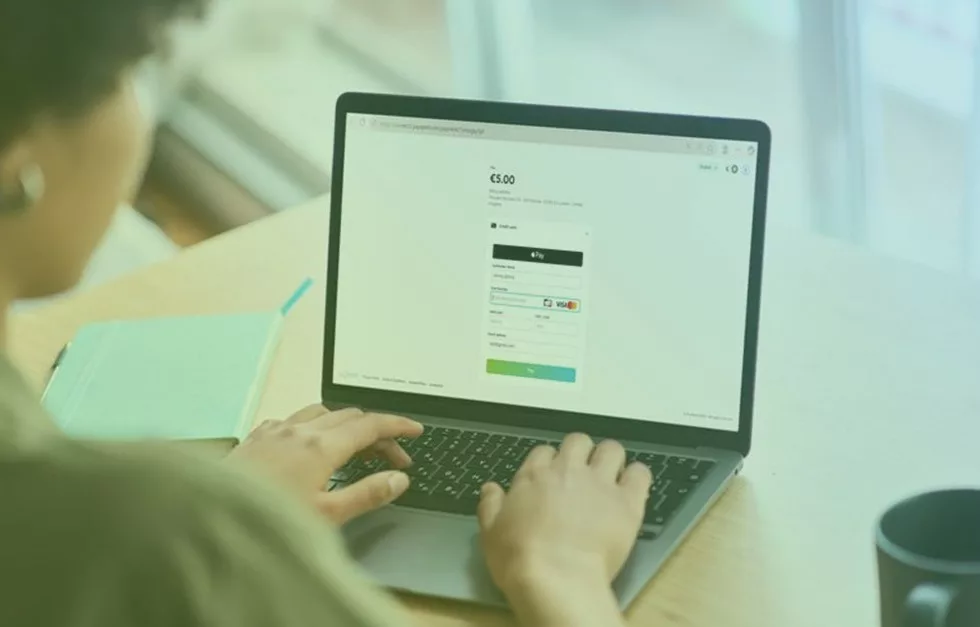

The ultimate goal of easy or automatic payment is to make the economic transaction as inexpensive as possible for the user, almost “invisible”. One method of implementing automatic payments is to include “buy” buttons on television or in Google searches, offering consumers the possibility of purchasing through electronic wallets or associated lenders (Marketplace Lenders or MPL). Accordingly, an “invisible” and direct link would be established between the main e-wallets, the cards associated with them and the users. From this future perspective, financial entities responsible for facilitate (both vendors and clients) payments through APIs and POS arise. In other words, it is software applied to points of sale (either physical or electronic commerce), which serves to create agile, secure and transparent payments for both parties to any transaction. This is the case of PayXpert, which offers innovative payment solutions so that merchants can grow sales, and users around the world have payment channels adapted to their currency, card and, ultimately, needs. With our worldwide network of local acquirers, we manage to optimize the number of successful transactions of our clients. Furthermore, we offer more than 20 alternative payment channels and work with 180 different currencies. Our objective is to develop the financial technology most adapted to the operation of the global economy, always focused on increasing the income of our clients.

“Conscious” financial technology for the well-being of people.

It is important to remember that the ultimate aim of financial technology is always to ease transactions between companies and users. The automation of payments is commonly associated with a lack of transparency by financial institutions, with a negative effect on the final consumer. The fact that users can make purchases without filling out forms, signing a receipt or choosing a credit card can cause the purchase process to become less conscious and deliberate. For that reason, this financial revolution must bring about a reformulation of how we conceive the purchasing process: we are talking about financial regulation tools helping users make conscious use of their spending level, and keep it within margins set by themselves. Automating payments should not mean the infringement of users, and fintech companies are not only perfectly aware of this, but are willing to collaborate in their protection. Companies like Credit Karma, Good Budget, Level Money (available on Google Play and Apple Store) or Mint are some of the entities that have appeared to turn automated payment into an easy and responsible payment.

Fintech revolution is the future of finance.

In conclusion, payment automation will involve the revolution in finance as we know them, helping users and firms save management time and money. It is about finding the perfect balance between increasing sales by companies, while promoting the conscious and responsible use of technology. It is everyone’s responsibility to know how to integrate these new tools, so that we can take advantage of all the potential benefits for the global economy. Fintech companies like PayXpert work to create conscious finances favouring both clients and companies.